Lind Capital Partners Municipal Market Commentary

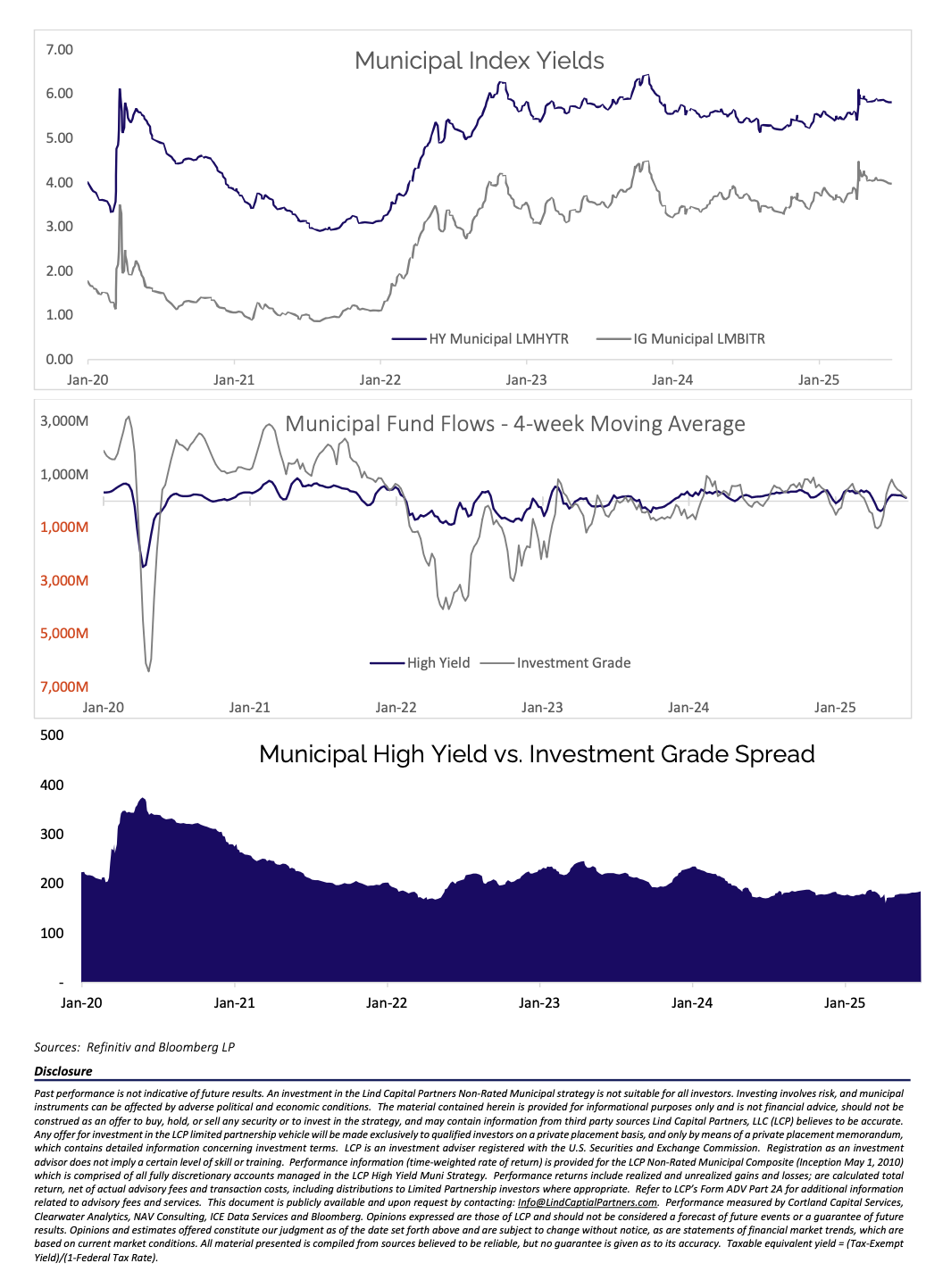

Municipal Market Performance and Benchmark Rates: The municipal bond market remained resilient in the face of elevated new issue supply in June. Both the investment grade (LMBITR) and high-yield (LMHYTR) indices returned 0.60% this month. Year-to-date, high-yield continues to outperform, albeit marginally, returning (0.39%) vs high-grade losses of (0.45%). The AAA municipal benchmark curve underperformed the Treasury market and bull-steepened in June as 5-year rates were lower by 15 bps versus 1bps out in 30 years. The slope of the US Treasury market curve remained largely unchanged as rates were roughly 15 basis points lower across the curve.

Mutual Fund Flows: The positive fund flow momentum experienced by mutual funds last month persisted in June as funds experienced their 9th straight week of inflows, although the inflow totals have consistently moderated. Total June inflows for investment grade and high yield funds totaled $615M and $522M, respectively. Year-to-date fund flows firmly favor high-yield, which have seen inflows totaling $4.4B. By comparison, investment grade inflows year-to-date total just under $2.2B. High-yield funds garnering over 70% of the total inflows this year despite representing only 15% of the overall municipal bond market speaks to the opportunity presented to and response by investors.

Primary Market Supply: Elevated new issue supply was the prevailing theme in June for municipal market participants. Total supply exceeded $65B, which is the highest monthly total since October 2024, when the catalyst was the looming Presidential election in November. June municipal supply was up ~25% MoM and YoY but over 40% higher versus the trailing 5-year average for the month. While high-yield new issue totals remain muted relative to trailing 5 and 10-year averages, especially when compared to the significant YoY increase in investment grade issuance this year, the pipeline of attractive non-rated deals remains strong. LCP purchased two-new issues in the final week of June at 7.00% (tax-exempt). While the primary market will understandably slow down ahead of Independence Day, the forward calendar continues to build in July, indicating continued opportunity.

Lind Capital Partners Municipal Non-Rated Market Commentary

Some themes are worth repeating, even for long-time LCP investors who are familiar with our strategy and the non-rated municipal market. Recently, we’ve had many conversations around seasonality in our market and how informed investors can incorporate these factors into investment decisions. To reiterate a few basics: the municipal market is heavily supply and demand driven. Supply in our market can be measured by the amount of primary issuance volume coming to market (i.e. how much new debt is being issued). Supply volume is dictated by the issuance process and the activity of the underwriting community, as well as macroeconomic factors. Demand can be measured by fund flows in and out of mutual funds and ETFs. The municipal market is largely dominated by retail investors. Predicting the whims of the retail investor is a fool’s errand, but fund flow data provides a reasonable leading indicator for demand; whether funds and ETFs will have available capital to deploy or may be forced sellers in the market. Another measurable demand factor is timing of coupon and principal payments and subsequent reinvestment of those cash flows.

Supply and demand can often be driven by external factors, such as the “Liberation Day” volatility we noted in our May commentary (May 2025 Note), which are difficult to predict. However, there are also several measured, repeating seasonal patterns that have held relatively consistent over time (see table below). We are entering a period, during the summer months, in which demand historically outweighs very limited supply, resulting in a supportive performance environment but more limited investment opportunities. This is an excellent time for investors to start making portfolio adjustments or taking care of operational tasks to prepare to deploy new capital during the most attractive purchasing period, historically, between Labor Day and Year End (September 2024 Note). Advisors can take advantage of summer meetings to have conversations with their clients about making decisions ahead of Q4.

We believe these historical trends are likely to continue this year, with one caveat. Over the past few months, we have seen heavy new issue supply. This has caused many new deals to be postponed after failing to gather sufficient investor appetite. After market participants return from Fourth of July week vacations, we expect healthy volume will also return. With higher supply than normal, we expect to see more market activity and more opportunities than historical trends would suggest. So… while preparing for the Q4 buying environment is still a prudent use of time, opportunistic investors with capital ready to deploy could take advantage of a few “bonus”weeks of investment opportunity in July in this year.

Lind Capital Partners Non-Rated Municipal Strategy

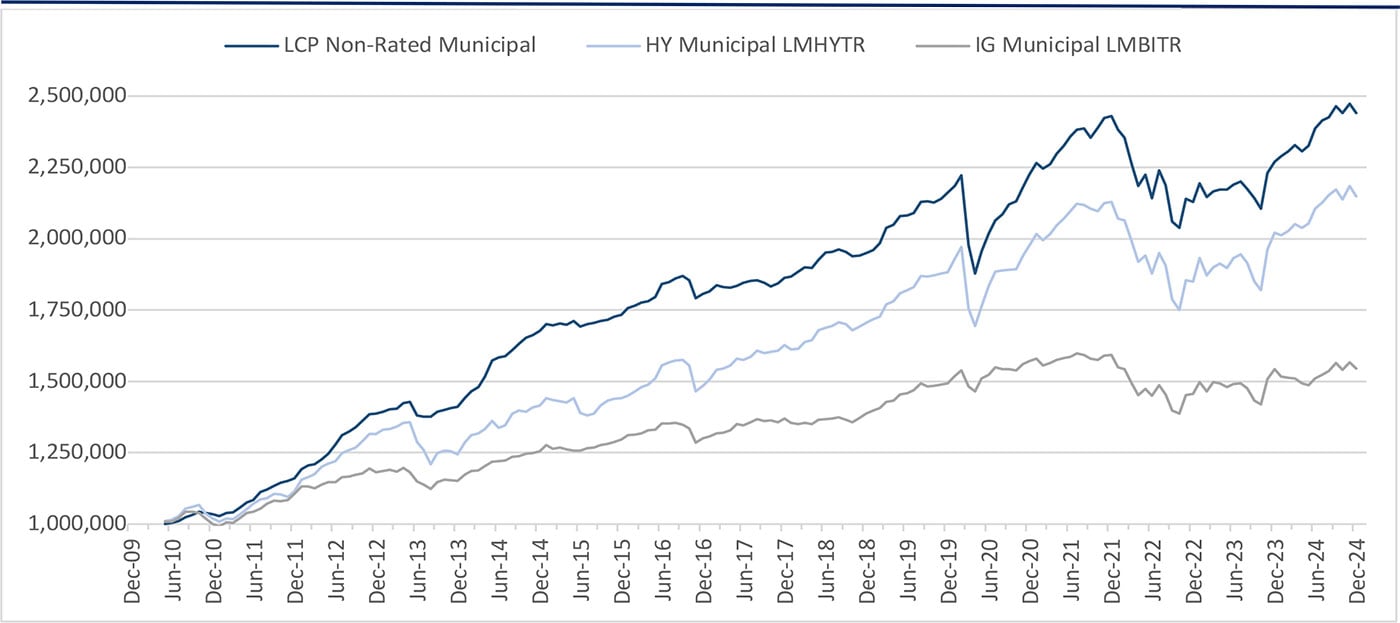

The chart above shows the increase in value of $1,000,000 invested in the LCP composite at inception (net of management fees and expenses) vs. the benchmark, the Bloomberg High Yield Muni (LMHYTR) as well as the Bloomberg Muni (LMBITR) indices (it is not possible to invest in either Bloomberg Index). Please contact us with questions regarding credit profile, returns, taxable equivalent yields or further portfolio information. Past performance is not indicative of future results.

Sources: Refinitiv and Bloomberg LP